RECENT SEARCHES

TRENDING SEARCHES

- Key Benefits

- Interest Rates

- Calculators

- Documents Required

- FAQs

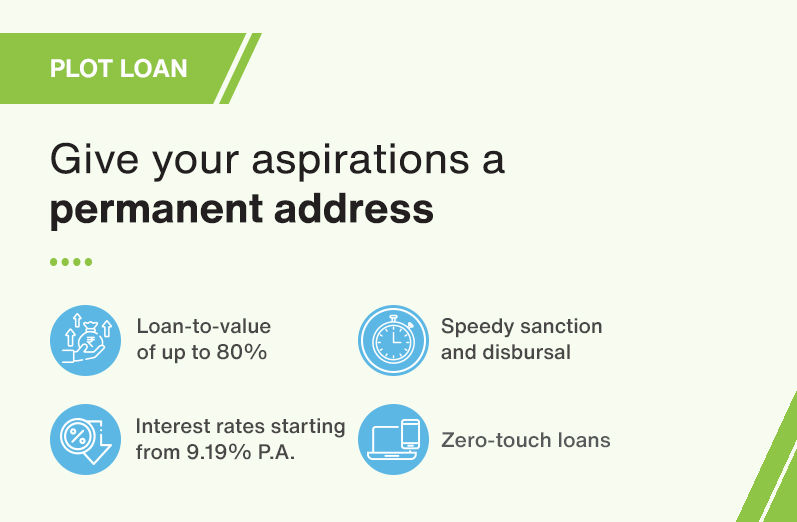

- Key Benefits

- Lower EMI Payments with interest rates starting from 9.19%

- Get quick sanction and disbursal with minimum documentation

- Loan to Value of Up to 80%

*T&C Apply

RESIDENT

Salaried

NON-RESIDENT INDIAN

Salaried

BUSINESS

Self Employed

PRACTICING PROFESSIONALS

Self Employed

*T&C Apply

Calculate Your Savings

- Emi Amount

- Loan Eligibility

- Tax Saving

Loan Tenure

Your Monthly EMI

₹

For the year at the % of interest rate

Total Interest Payable

₹

Total Payment (Interest + Principal)

₹

Loan Tenure

Your EMI Will Be

₹

Your Eligibility

₹

Financial Details

Income Tax Benefits

₹

Income Tax Payable includes 4% cess.

Income Tax Payable After Loan

₹

Income Tax Payable Before Loan

₹

- Salaried

- Self-Employed

- Practicing Professional

- Salaried NRI

Pan Card or Form 60 is a mandatory requirement for the loan application processing

For Proof of Identity and Address, any one of the below documents is acceptable

- Proof of possession of Aadhaar number

- Valid Passport

- Valid Driving License

- Voter’s Identity Card

For Income Documents, we accept

- Latest 1 month salary slip, or a Salary Certificate authorized by the signatory of the company on the letter head

- Proof of employment for 2 years (Form 16 or Joining date on salary slip or employer letter or appointment letter etc.)

- Last 6 months statement of bank account where salary is credited

- Proof of bonus of last 2 years or Variable incentive for last 6 months – Bank statement reflecting the credits and salary slip letter reflecting bonus or variable incentive

- Bank statement reflecting EMI clearance of Last 6 EMIs OR Statement of account

- Sanction letter to evidence Collateral address

- Customer declaration for - Loan outstanding & List of documents submitted.

For Under construction Home Loans – Approved Projects

- Allotment Letter or Stamped Agreement for Sale

- Payment Receipts or bank account statement showing all payments made to the Builder

For Resale Home Loans

- Current Registered or Draft Agreement for Sale (only for Maharashtra) or Allotment Letter or Stamped Agreement for Sale

- Prior Chain Link title documents

- Occupancy Certificate (in case property is ready) or Approved Plan copy (photocopy of the blueprint)

- Share Certificate (only for Maharashtra), Maintenance Bill, Property Tax Receipt

- Payment Receipts or bank account statement showing all the payments made to Seller

- Pan Card or Form 60 is a mandatory requirement for the loan application processing

- Proof of identity (Aadhaar number/ Valid Passport/ Valid Driving License / Voter's Identity Card)

- Proof of Address (Aadhaar number/ Valid Passport/ Valid Driving License / Voter's Identity Card)

- ITR and Financial statements including P&L, Balance Sheet, COI & Schedules - 2 Years - certified by a Chartered Accountant

- Bank Statements for last 12 months

- Business Continuity Proof for 5 years

- Tax Audit Report, if applicable

- Bank statement reflecting EMI clearance of Last 6 EMIs OR Statement of account

- Sanction letter to evidence Collateral address

- Customer declaration for - Loan outstanding & List of documents submitted.

For Under construction Home Loans – Approved Projects

- Allotment Letter or Stamped Agreement for Sale

- Payment Receipts or bank account statement showing all payments made to the Builder

For Resale Home Loans

- Current Registered or Draft Agreement for Sale (only for Maharashtra) or Allotment Letter or Stamped Agreement for Sale

- Prior Chain Link title documents

- Occupancy Certificate (in case property is ready) or Approved Plan copy (Xerox Blueprint)

- Share Certificate (only for Maharashtra), Maintenance Bill, Property Tax Receipt

- Payment Receipts or bank account statement showing all the payments made to Seller

- Pan Card or Form 60 is a mandatory requirement for the loan application processing

- Proof of identity (Aadhaar number/ Valid Passport/ Valid Driving License / Voter's Identity Card)

- Proof of Address (Aadhaar number/ Valid Passport/ Valid Driving License / Voter's Identity Card)

- ITR and Financial statements including P&L, Balance Sheet, COI & Schedules - 2 Years - certified by a Chartered Accountant

- Practice Continuity Proof for 5 years

- GST challans for last 1 or 2 or 3 quarter since filing of last returns

- Tax Audit Report, if applicable

- Bank statement showing Rental credits & Registered Rent Agreement, if applicable

- Bank statement reflecting EMI clearance of Last 6 EMIs OR Statement of account

- Sanction letter to evidence Collateral address

- Customer declaration for - Loan outstanding & List of documents submitted.

For Under construction Home Loans – Approved Projects

- Allotment Letter or Stamped Agreement for Sale

- Payment Receipts or bank account statement showing all payments made to the Builder

For Resale Home Loans

- Current Registered or Draft Agreement for Sale (only for Maharashtra) or Allotment Letter or Stamped Agreement for Sale

- Prior Chain Link title documents

- Occupancy Certificate (in case property is ready) or Approved Plan copy (Xerox Blueprint)

- Share Certificate (only for Maharashtra), Maintenance Bill, Property Tax Receipt

- Payment Receipts or bank account statement showing all the payments made to Seller

- In case of Indian Passport Holder- Certified copy of Valid Indian Passport along with copy of valid visa copy or work or residence permit copy.

- In case of Foreign Passport holder, copy of valid Foreign Passport along with OCI (Overseas Citizen if India) card or PIO (Person of Indian Origin) card.

For Income Documents, we accept

- Latest 3-month salary slip, or a Salary Certificate authorized by the signatory of the company on the letter head

- Proof of employment for 5 years (Tax returns or Employment contract or Joining date on salary slip or employer letter or appointment letter etc.)

- Last 6 months statement of bank account where salary is credited and last 6 months NRE or NRO bank statement.

- Latest valid Contract Copy and / or appointment letter

- Complete Continuous Discharge Certificate (CDC) for employees working on Ships

- Overseas Credit Bureau report not older than 30 days

For Under construction Home Loans – Approved Projects

- Allotment Letter or Stamped Agreement for Sale

- Payment Receipts or bank account statement showing all payments made to the Builder

For Resale Home Loans

- Current Registered or Draft Agreement for Sale (only for Maharashtra) or Allotment Letter or Stamped Agreement for Sale

- Prior Chain Link title documents

- Occupancy Certificate (in case property is ready) or Approved Plan copy (Xerox Blueprint)

- Share Certificate (only for Maharashtra), Maintenance Bill, Property Tax Receipt

- Payment Receipts or bank account statement showing all the payments made to Seller

*Disclaimer: All contents mentioned on this page, including but not limited to documents, eligibility may vary for each borrower and are subject to the discretion of the lender. The content is subject to change without prior notice.

- Plot Loan

- Plot Loan Process

- Plot Loan Terminology

- Important Documents

- Charges Related

- Insurance Related

A Plot loan is an amount of money that a person borrows from a financial institution to purchase a plot of land for the construction of a residential unit on the same. This loan is at a certain rate of interest for a particular number of years (tenure), which is to be paid back in equated monthly instalments (EMI).

There are a few conditions that need to be met for Plot loans,

The residential plots for construction otherwise allocated by the builders are to be approved by Godrej Capital

The plot should be clearly identifiable and demarcated

Step 1: Submit your Application

Your loan application should include a duly filled in loan application form, proof of income, proof of identity and proof of address.

Step 2: Application Evaluation and Loan Sanction

Our internal team promptly evaluates and processes the loan application for loan sanctioning.

Step 3: Property valuation

After receiving the property papers, we conduct a legal and technical valuation of the plot to ensure compliance. Upon approval, we proceed with the loan disbursal process. The process is simplified if you are purchasing a home from an approved project.

Step 4: Loan Disbursal

After obtaining the necessary approvals, the loan agreement is signed, and the loan amount is disbursed.

A financial institution undertakes certain risks while lending money to borrowers, so for prudent lending, the institution checks the repayment capacity of the borrower through his/her savings, income, age, qualifications, nature of work, any loans currently served etc. This is called Credit Evaluation and determines the loan eligibility comprising of the loan amount, tenure of the loan and the rate of interest.

A financial institution empanels agencies for objective valuation of the property it takes against the loan as security. The valuation is based on its age, usage, legal documentation, Construction cost, as well as its geographical location. Market conditions also come into play, including whether there is a high demand for that particular type of property in the area in which it is located.

Registration of a property includes necessary stamping and paying of registration charges (may vary from state to state) for a sale deed and getting it recorded at the sub-registrar's office of the concerned jurisdictional area.

If someone is the co-owner of the property in question, it is necessary that he/she also be the co-applicant for the home loan. In case of sole ownership of the property, any member of your immediate family can be a co-applicant. If joint income is considered to arrive at eligibility, the second person needs to come in as a co-applicant.

National Automated Clearing House (NACH) is a centralized structure created to make payments more accessible and cost-effective; NACH offers a fast and efficient clearing platform. The NACH debit mandate is used by GHF to automatically deduct monthly instalments from your bank account for the loan availed.

Two ways to cancel your NACH mandate are:

You can log in to the Customer Portal and request to cancel the mandate through the Write to Us section.

You can also send an email to customercare@godrejhf.com through registered email ID or call our Customer Care +91 22 68815555 through a registered mobile number and place a request for NACH mandate cancellation.

You need to mention the Loan Account Number (LAN) in the request, and our team will connect with you within 48 hrs.

The processing fee is a one-time charge paid by the borrower to the financial institution to cover expenses associated with processing a loan application.

A loan sanction letter is issued by a financial institution post evaluation of an applicant’s creditworthiness and other details like KYC etc. This letter is proof of eligibility of a loan from the financial institution and mentions the main loan details like maximum loan amount, maximum tenure, type of rate of interest, EMI amount and special conditions, if any. A sanction letter with these conditions is valid for a specified period of time.

A Power of Attorney allows a person to grant another person the right to make decisions regarding the person's assets, finances and real estate properties.

There are two types of power of attorney.

First, the 'General Power of Attorney' where a property owner confers 'general' rights. The rights include but are not limited to sell, lease, sub-lease etc.

Second, is the 'Special Power of Attorney' wherein only a specific right is given by the owner to the chosen person.

The EMI is the amount of money a borrower pays back to a financial institution on a monthly basis towards the loan availed. It comprises of 2 components – the principal and the interest. So with every EMI, the borrower pays back a portion of the loan amount as principle and a certain amount of interest.

The EMI amount remains constant and by the end of the tenure, the borrower has paid back both principal and interest amount in full. At Godrej Capital, you can avail product variants where we give you a break from your EMI when you need it the most. Read more here.

Pre-EMI is the interest amount paid by the borrower till the time final disbursement is pending and EMI is initiated. It is the interest on the amount of the loan disbursed and is payable every month from the date of each disbursement up to the date of commencement of the EMI. Pre-EMI is mostly applicable in cases where Under Construction property/Plot + Construction loans during the construction stage being purchased on loan.

The time period (in months or years) for which a financial institution lends the money to a borrower. The tenure may be different from borrower to borrower

At Godrej Capital, Plot + Construction loans come for tenures up to 15 years.

The rate of interest is the percentage of principal charged by a financial institution from its borrower for the money lent. It is paid over and above the principal amount borrowed.

There are 2 types of rate of interests

Floating Rate of Interest – The rate moves up and down with an index, at Godrej Housing Finance, all floating rate of interest loans are pegged to GHF PLR – Godrej Housing Finance Prime Lending Rate. The rate varies over the repayment tenure of the loan

Fixed-Rate of Interest – The rate remains the same for the entire repayment tenure of the loan.

Collateral is an asset (the plot) a financial institution accepts and keep as security for a loan it extends till the loan is fully repaid. This helps the financial institution to cover its risks.

APF stands for Approved Project Funding.

Godrej Capital identifies projects by certain developers and builders and evaluates basis the properties’ legal and technical evaluation. If a project qualifies the necessary requirements, it’s included in the APF master of Godrej Capital.

The TAT(turn around time) for a loan disbursal, is lesser, where a project is already an APF and the loan processing is much simpler

Loan to Value (LTV) is the amount of loan divided by the total value of the property and is represented in %. Loan value of INR 75 lakhs for a property worth INR 1 Crore would mean 75% LTV.

Own Contribution or OCR is the same as a down payment. It is the difference between the loan amount Godrej Capital (or any financial institution) will provide and the total value of the property.

At Godrej Housing Finance, we make OCR a breeze with Easy Down payment options we call Parallel Funding, where a borrower doesn’t get burdened and pays the down payment in parts on a pro-rata basis. This enables the borrower to buy his/her dream home sooner than he/she normally would.

OCR and down payment are also referred to as ‘Margin’ money.

The documents relating to transfer, sale, lease or any other form of disposal of immovable property. Registration is compulsory by law for all properties under Section 17 of the Indian Registrations Act, 1908. Once a property has been registered lawfully, it means that the person in whose favour the property has been registered is the lawful owner of the premises and is fully responsible for it in all respects.

Disbursement means paying out the loan amount to the borrower or the builder from which the borrower has bought the home. The disbursement can be either in full or in tranches depending on the type of home financed (tranches are common for under-construction properties) and the terms agreed between the financial institution and the borrower.

The Schedule of Charges is the list of charges and corresponding amount levied by a financial institution over the duration of the loan, if applicable. For Godrej Housing Finance, refer to the schedule of charges here.

Statement of Account for a loan details out all the transactions completed in a particular loan account date by date. It also shows the outstanding balance due, the interest rate charged on that outstanding balance and any fees/charges incurred.

Most Important Terms and Conditions details out the Loan details, repayment schedule, schedule of charges and any other relevant details of a loan account which a borrower must know.

A repayment schedule is a table of detailed loan payments for every period, showing the amount of principal and the interest that comprise each payment until the loan is fully paid off.

An Interest Certificate is a legal document issued by the lender which details out the bifurcation of the Principal and Interest Amount paid towards a home loan account in a particular financial year. The same is used for taxation purposes.

The NOC, or No Objection Certificate, is a legal document that states that you have paid all the EMIs and cleared all other outstanding loan dues and is issued by the company post the closure of the loan account

Bounce charges are incurred if the EMI is not paid by the borrower on the due date.

Late Payment charges, also referred to as ‘Penal charges’ are the charges incurred on the late payment of the outstanding dues in case of EMI bounce, by the borrower.

Swap charges are incurred by the borrower for changing the repayment instrument or change in the bank account for NACH Mandates.

Recovery charges are levied by the Company for any expenses incurred on collection of overdue from the borrowers

Foreclosure or prepayment charges are the charges a borrower incurs for closing the loan ahead of its full loan term. In case of Individual loans with floating rates, there are no foreclosure or prepayment charges. For Individual loans with fixed rates, there are no foreclosure or prepayment charges if the payment is through own source of funds. However, if the loan is closed through other financier, then charges will be applicable as per the Schedule of Charges by the lender.

For all Non-Individual loans, foreclosure, prepayment charges are as per the Schedule of Charges shared by the lender.

No, it is not mandatory to obtain Insurance. However, Insurance is a voluntary risk mitigation device that helps customers in multiple ways, such as securing the asset, helping in paying off the loan liability in an unlikely event.

The insurance contract is between the Insurer and the customers. The company plays a limited role in facilitating the insurance contract between customers and Insurers. It will be the Insurer's responsibility to provide details and benefits to the customers.

Loan-linked Insurance covers a large amount of the loan liability. In any unforeseen circumstances like death, disability, hospitalization, and diagnosis of critical ailments, the Insurer can repay the loan liability through Insurance.

Credit-Life Insurance provides death cover for natural, accidental, and unnatural cause deaths. It also includes coverage for death due to Covid-19 and can be extended to co-borrowers. Customers can also avail the benefit of Section 80-C Income Tax deduction

Survival-Benefit Plan is for critical illness insurance and provides additional cover for medical emergencies like heart attack, stroke, or cancer. Because these emergencies or illnesses often incur greater than average medical costs, these policies pay out cash to help cover those overruns where traditional health insurance may fall short. These policies come at a relatively low cost. However, the instances that they will cover are generally limited to a few illnesses or emergencies.

Health insurance aims to provide a defence against the hardship caused due to lack of income because of (a) Disease, (b) Accident, (c) Surgery and (d) hospitalization.

Property Insurance secures the property for which the loan has been availed; ensures the security of valuables within the house. It is applicable for entirely constructed property wherein the customer has possession of the property. The Claim amount is the reinstatement value of the property.

Other Products